Self-Employed Mortgages · Calgary & Alberta

Self-Employed Mortgage Calgary — Your Bank Said No. We Have 50+ Other Options.

Banks use your declared income. A broker accesses lenders who look at gross income, bank statements, and real cash flow. If you've been told no — that's one lender's answer, not the market's.

- A, B, and alternative lenders — including specialists in self-employed income

- Qualify with 1 or 2 years self-employed depending on your profile

- Tax write-offs can be added back — doesn't have to hurt your application

- Free service — broker fee paid by lender

Your Bank Said No — That's Not the End

Banks are A-lenders with the strictest qualification criteria. Most self-employed borrowers rejected by their bank qualify somewhere in the B-lender or alternative lender stack. A bank shows you one door. A broker opens fifty.

Why Banks Struggle With Self-Employed Borrowers

The same financial discipline that makes you a good business owner makes you look unqualifiable to a bank.

How Your Bank Sees You

- Uses your declared net income — the NOA number after all write-offs

- That number is deliberately minimized to reduce your tax bill

- Which makes you look unqualifiable on paper

- One qualification method. Take it or leave it.

How a Broker Approaches It

- Shops A, B, and alternative lenders — each with different income methods

- Some lenders allow adding back non-cash expenses (CCA, depreciation)

- B-lenders can qualify on bank statement cash flow

- Matches your profile to the right lender before you apply

How Self-Employed Income Actually Works for Mortgages

Three qualification methods — lenders use different ones. Most borrowers only know about the first.

Traditional Qualification (A-Lenders)

Banks & major lenders- 2-year average net income from T1 generals and NOAs

- Line 15000 minus business expenses

- Best rates — but strict. Works if declared income is strong.

- Most major banks use only this method

Gross-Up / Add-Backs

Broker-accessed A/B lenders- Lenders add back depreciation, CCA, non-cash expenses

- CMHC allows 15% gross-up on gross income for qualifying

- Increases qualifying income without changing your tax situation

- Available only through brokers — banks don't offer this

Stated / Bank Statement Income (B-Lenders)

Bridge strategy- Qualifies on stated business income with supporting documents

- Bank statements, GST returns, business financials

- Higher rate than A-lender — but accessible without 2 years of strong NOAs

- Bridge strategy: qualify now, refinance to A-lender in 2 years

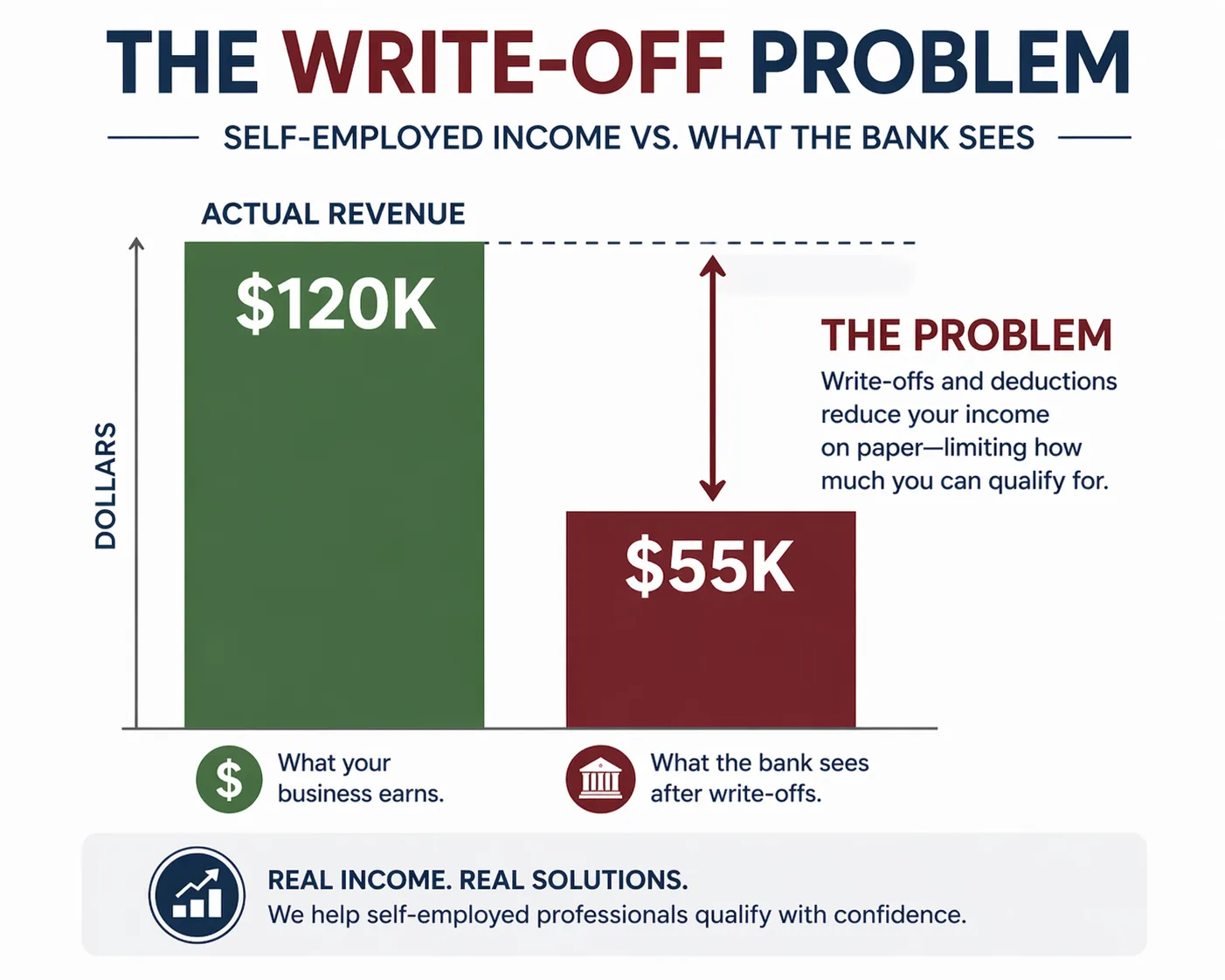

The Tax Write-Off Problem — and the Four Solutions

The most common pain point for self-employed Calgary homebuyers.

The conflict in plain terms:

You claim every legitimate expense. Your taxable income is low — correct from a tax perspective. Then you apply for a mortgage and your bank says you don't qualify. The same discipline that reduces your tax bill is being used against you.

Gross-up / add-back approach

Work with a broker who accesses lenders that allow adding back non-cash expenses — depreciation, CCA, vehicle allowances. Your qualifying income increases without touching your tax return.

B-lender with bank statement income

Your bank statements prove what's actually moving through your business — and that's what the lender qualifies on. Real cash flow, regardless of declared income.

Plan ahead before filing taxes

If you're buying in 1–2 years, consider drawing a higher salary and paying more tax in exchange for better mortgage qualification. A broker and accountant can run this calculation together.

Co-applicant with T4 income

If a spouse or partner has salaried income, combining applications opens A-lender doors. The T4 income anchors the application, your business income supplements it.

The 2-Year Rule — And the Real Exceptions

Standard is 2 years. But there are real paths for people who don't meet it.

Less than 2 years, strong income, same field

A-lender possibleSome lenders will consider 1 year if you have strong financials and were previously employed in the same field. Your industry track record matters as much as your business age.

Previously T4 employee, now incorporated

Viewed very favourablyMany lenders view this as a career progression, not a risk. You have a track record — just a different legal structure. This is one of the strongest self-employed applications.

Less than 1 year in business

B-lender territoryPossible at higher rates through B-lenders. Plan the exit: 2-year track record, then refinance to A-lender at renewal.

Applied to the wrong lender directly

Wasted credit hitThe biggest mistake. A hard inquiry on your credit file wasted on a lender that would never approve you. A broker pre-qualifies you with the right lender before submitting anything.

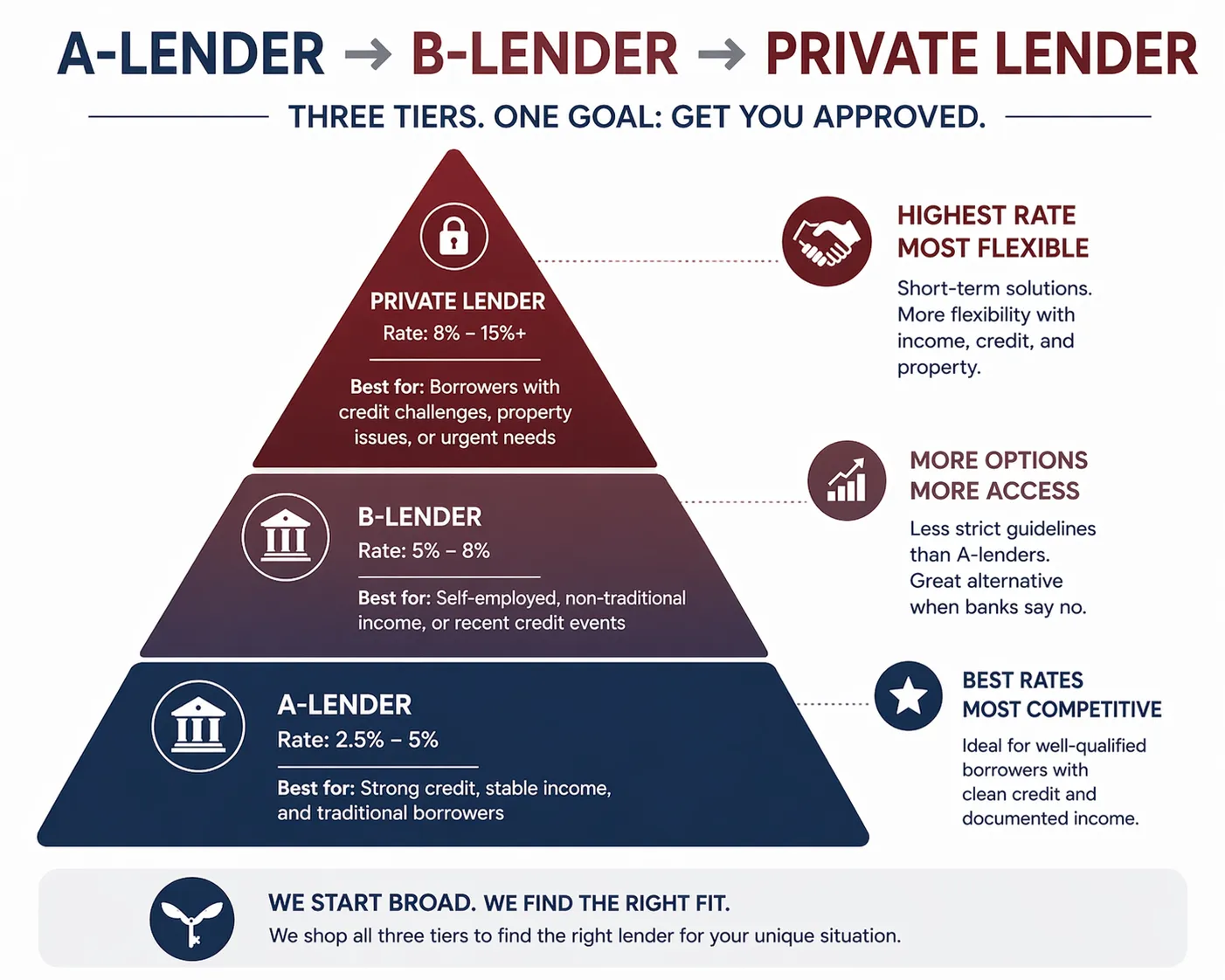

A-Lender vs B-Lender vs Private — What's the Difference?

Three tiers. You're not stuck with just the one your bank offers.

A-Lenders

Best ratesBanks, Credit Unions, Monolines

- Best rates — strictest qualification

- 2 years strong declared income required

- 680+ credit score typically

- Goal: get here at renewal if you start elsewhere

B-Lenders

Bridge strategyHome Trust, Equitable Bank, Bridgewater, CMLS

- 0.5–1.5% above A-lender rates

- Flexible on income documentation

- Accept stated income with supporting docs

- Most self-employed borrowers qualify here first

Private Lenders

Last resortMICs, individual investors

- 6–12%+ rates currently

- Minimal income documentation

- Short terms (1–2 years)

- Exit strategy is non-negotiable before signing

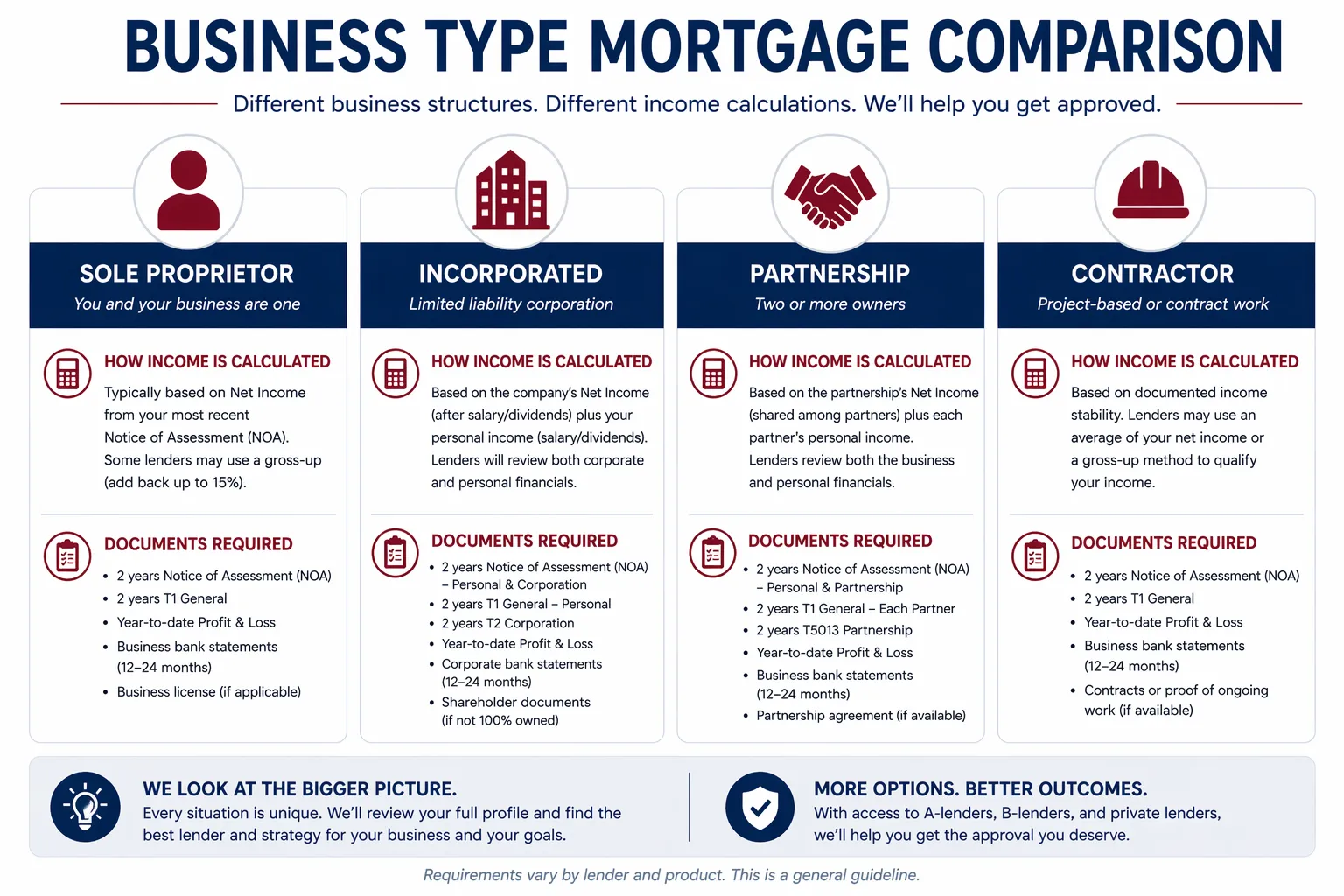

Your Business Type — How Each Is Handled

Sole proprietors, incorporated owners, contractors, and commission earners all qualify differently.

Sole Proprietor / Freelancer

- Income from Schedule C on T1 general

- Lenders see net income after business expenses

- Gross-up strategies help — adding back non-cash expenses

- Straightforward A-lender path if declared income is strong

Incorporated Business Owner

- Lenders look at salary drawn, dividends, and retained earnings

- Salary drawn is cleanest — most straightforward to document

- Dividends usable but require 2 consistent years at most lenders

- Retained earnings don't count unless you can demonstrate access

Contractor (T4A Income)

- Treated similarly to self-employed by most lenders

- Long-term stable contracts = strong application

- A-lender path available with 2 years T4A history

- Some lenders want a letter confirming ongoing contract relationship

Commission Income

- 2-year average of T4 box 42 income used

- Growing commission income viewed more favourably

- Stability and trend matter as much as amount

- A-lender path if 2-year average qualifies

Documents You'll Need

Requirements vary by lender tier. B-lenders need less paperwork — and are often more accessible.

For A-Lender Qualification

- 2 years T1 generals (full tax returns)

- 2 years NOAs (Notice of Assessment from CRA)

- Business registration or articles of incorporation

- 3 months business bank statements

- Current year income confirmation

For B-Lender / Stated Income

- 6–12 months business bank statements

- Business license or registration

- GST/HST returns showing revenue

- Accountant letter (sometimes required)

- Less paperwork, more income flexibility

One gap self-employed borrowers often miss at closing

You have no employer-provided disability or life coverage. If your income stops, your mortgage doesn't. Frank Cover is a Calgary-based independent insurance broker who specializes in income protection and mortgage coverage for self-employed and incorporated professionals — the same clients a mortgage broker serves.

Frequently Asked Questions

Self-Employed Mortgage Guides

Deep-dive articles on every aspect of qualifying as a self-employed borrower in Calgary and Alberta.

How to Get Approved — 2026 Guide

Full overview: who qualifies, how lenders evaluate self-employed income, and your options.

Income Requirements Explained

How different lenders calculate your income — and why the same income qualifies differently.

1 Year Self-Employed — Can You Get Approved?

Don't wait unnecessarily. Lenders that work with 1 year of history and how to qualify.

How Write-Offs Affect Mortgage Approval

The write-off conflict explained — and how to solve it before applying.

Documents Checklist (Alberta Guide)

Exactly what to prepare for A-lender and B-lender applications.

What income will a lender actually use?

Enter your NOA income and add-backs — see your real qualifying income.

Self-Employed in Calgary? See What You Actually Qualify For.

A bank shows you one door. A broker opens fifty. Free consultation — no obligation.