Bad Credit Mortgages · Calgary & Alberta

Bad Credit Mortgage Calgary — You Still Have Options

Banks aren't the only mortgage lenders in Canada. B-lenders and private lenders approve where banks don't — and a broker builds the plan to get you to better rates at renewal.

- B-lenders approve from 560 credit score with 20% down

- Private lenders available regardless of credit history

- Clear path to A-lender rates at renewal — ~$550/month savings on $500K

- One application, right lender — no multiple credit hits

Non-judgmental. Confidential. No obligation.

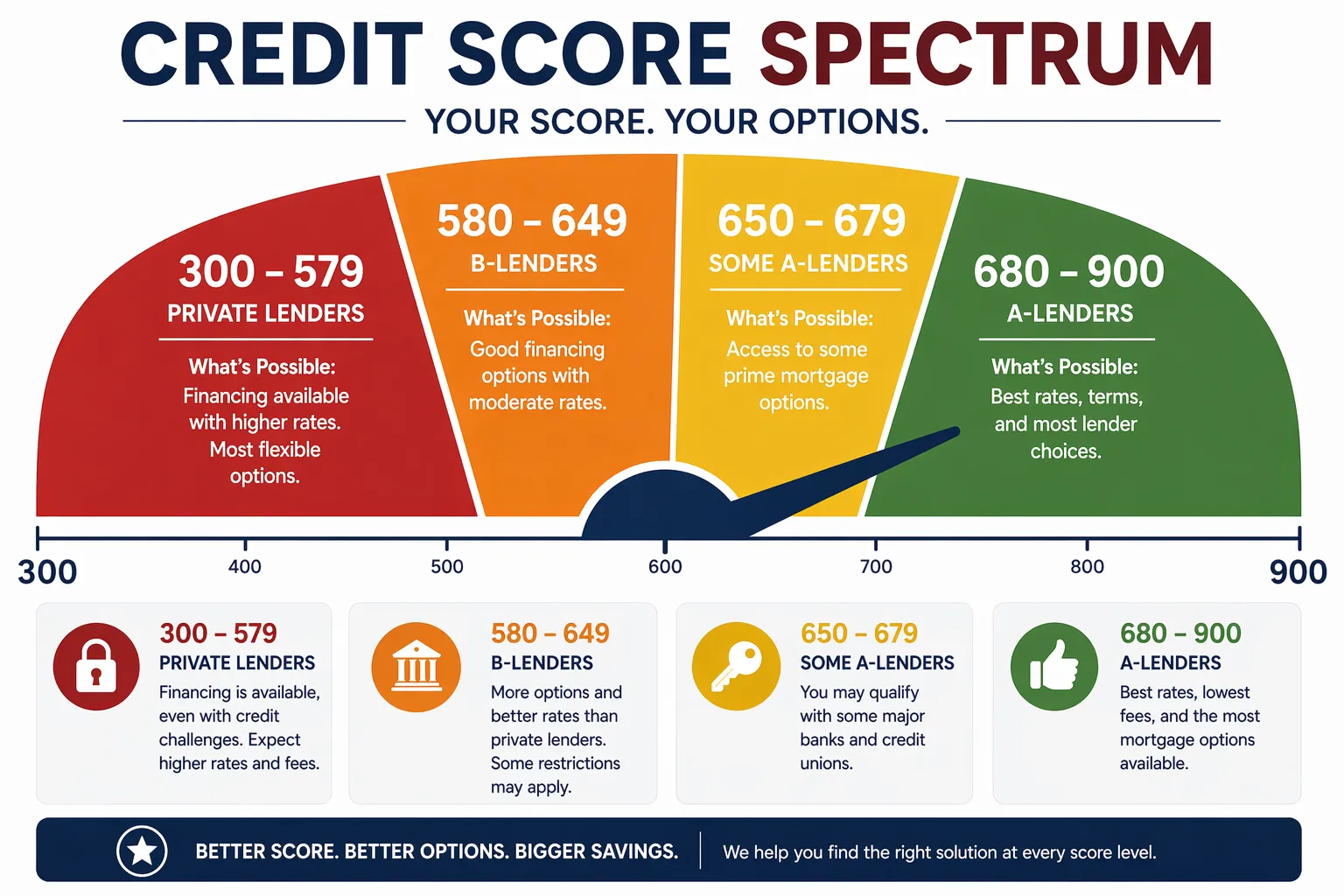

Can I Get a Mortgage With Bad Credit in Calgary?

Yes — with conditions. Here's what's available at each credit score level.

A-lender possible

Larger down payment or co-signer can help. Standard path with some conditions.

B-lender territory

Real mortgages, real homes, higher rate. Designed as a bridge to A-lender. Most common path.

B-lender with strong factors, or private

Large down payment and stable income can offset the score. Private lenders available.

Private lender

Short term, higher rate — but a clear path back to normal exists with an exit plan.

The rate you get isn't permanent.

The goal is to get into homeownership, rebuild credit during your mortgage term, then refinance to a better rate at renewal. A broker builds this plan upfront — you know exactly what the path looks like before you sign anything.

What Credit Score Do You Need?

A direct answer — not a calculator, not a phone call requirement.

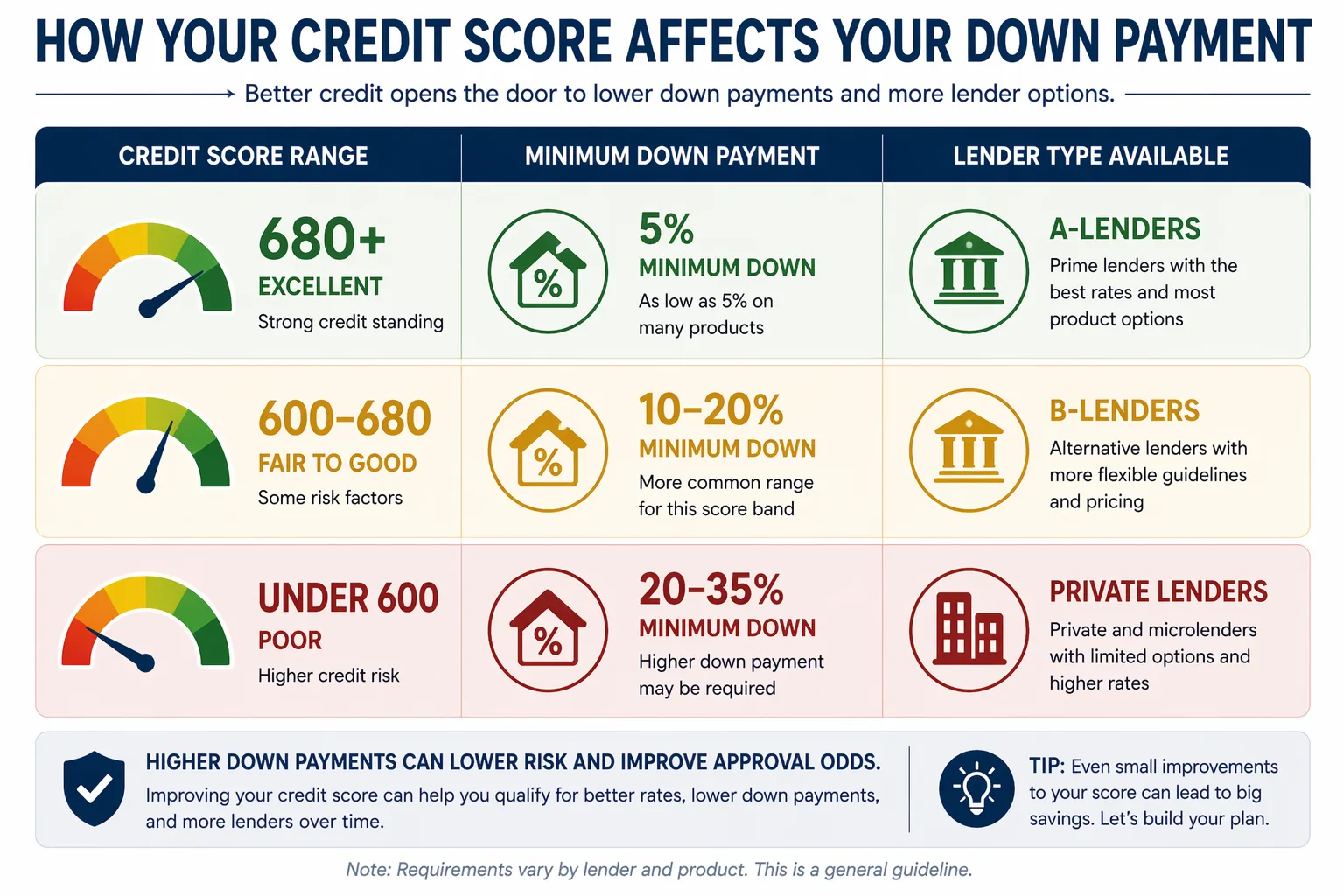

| Credit Score | What's Available | Min. Down Payment |

|---|---|---|

| 680+ | A-lender, best rates | 5% minimum |

| 640–679 | A-lender, most lenders | 5–10% |

| 600–639 | B-lender, some A-lenders | 10–20% |

| 560–599 | B-lender | 20%+ |

| 500–559 | B-lender (strong file) or private | 20–25% |

| Below 500 | Private lender | 25–35% |

Credit score is one factor. Payment history, employment stability, down payment size, and what caused the low score all matter. A 580 from a medical emergency 2 years ago is treated very differently than a 580 from ongoing missed payments.

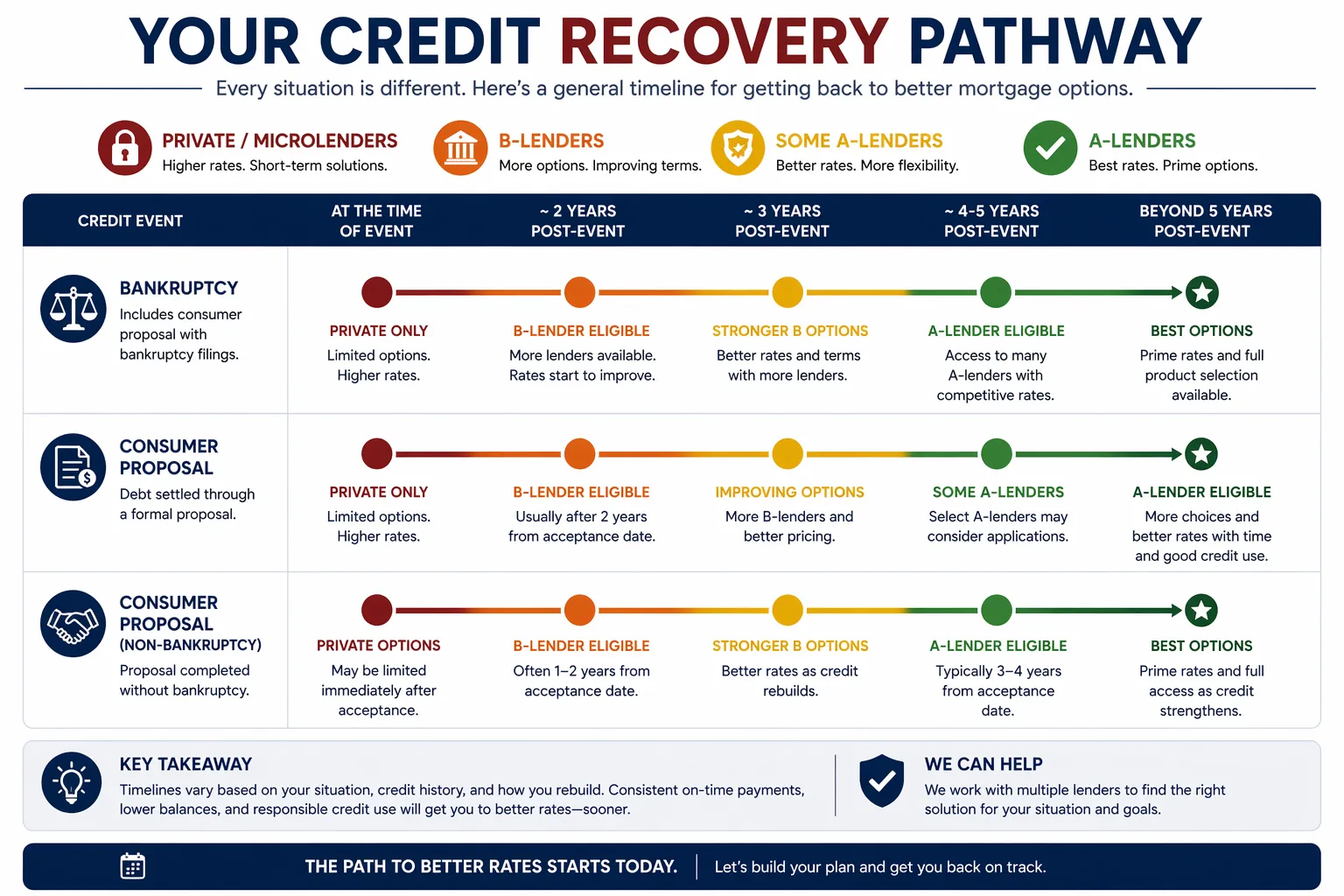

Your Specific Situation — Waiting Periods and Paths

Each credit event has different timelines and different lender options.

After Bankruptcy

Immediately post-discharge — 25–35% down required

1 year post-discharge with strong compensating factors

2 years post-discharge with rebuilt credit (650+)

Secured credit card immediately after discharge — use and pay monthly. Clock starts at discharge, not filing.

After Consumer Proposal

During or immediately after proposal with 20% down — full completion not always required

2 years after completion with 650+ credit score

Consumer proposals viewed more favourably than bankruptcy. On-time mortgage payments during a proposal count positively.

Collections on File

Most lenders overlook if score is otherwise acceptable

Must be addressed — lenders require payment before closing

Must be cleared before most lenders will approve — no exceptions

Late Payments

Minimal impact if score has since recovered

Significant impact — B-lender path with explanation letter

Most serious — flagged by all lenders, requires detailed explanation

After Foreclosure / Power of Sale

Immediately with strong equity position (35%+ down)

2–3 years with substantial down payment

Typically 5–7 years — Alberta allows deficiency pursuit, which affects credit severely

A-Lender vs B-Lender vs Private — Plain Language

Three tiers of mortgage lenders. You're not stuck with just the first one.

A-Lenders

Best ratesBanks, credit unions, major monolines

- Current rates ~4–5% for insured mortgages

- 620+ credit score minimum for most

- Clean recent credit history required

- Full documentation, standard qualification

B-Lenders

Bridge to A-lenderHome Trust, Equitable Bank, Bridgewater, CMLS, Haventree

- Rates typically A-rate + 1–2%

- Accept 560+ credit scores

- More flexible on recent credit events

- 20% down typically required

- 1–2 year terms — designed to transition

Private Lenders

Last resort with exit planMICs, individual investors

- Rates 7–12%+ currently

- Asset-based — property value matters more than credit

- Minimal income and credit documentation

- Short terms (6 months – 2 years)

- Exit strategy is non-negotiable before signing

The Recovery Path — Buy Now, Refinance Later

Homeownership is the starting point. Here's what the full path looks like — with real numbers.

Real Numbers — Calgary Example

Today

560 score

B-lender · 6.5%

$500K home

2 years later

655 score

A-lender · 4.5%

Home ~$530K

~$550/month saved · $33,000 over the next 5-year term

Based on standard Canadian amortization. Actual results depend on rates at renewal.

Year 0 — Get Into Homeownership

- B-lender or private mortgage secured

- Down payment in place

- Start building equity from day one

During Term (1–2 years)

- Every on-time payment rebuilds credit

- Pay down other debts aggressively

- Don't apply for new credit cards or loans

- Use secured credit card strategically

- Target: 640+ score before renewal

At Renewal (1–2 years later)

- Requalify for A-lender with 640+ and 24 months clean history

- Rate drops significantly (often 1–2% reduction)

- Home equity has grown — stronger application

- Monthly savings compound over the new term

Why a Broker for Bad Credit — Not a Bank

Banks will tell you no. That's not their fault — they only have A-lender products.

| Your Bank | A Mortgage Broker |

|---|---|

| One lender tier (A-lender only) | All three tiers — A, B, and private |

| "Sorry, we can't help you" | "Here's what's available and what the path looks like" |

| Multiple credit hits if you shop yourself | One application, right lender, first time |

| No plan for improving your situation | Full recovery plan before you sign anything |

| Costs nothing (but likely more long-term) | Free — lender pays the broker fee |

Down Payment by Credit Level

Documents Needed

- 2 years T4s or Notices of Assessment

- 3 months recent pay stubs

- Bank statements showing down payment

- Explanation letter for credit events

- Government-issued photo ID

The explanation letter matters more than people think. A well-written letter explaining what caused the credit problem and what's changed is standard for B-lender applications. It can make the difference between approval and decline. A broker helps you write it correctly.

Frequently Asked Questions

Bad Credit Mortgage Guides

Deep-dive articles on getting a mortgage with bad credit in Calgary and Alberta.

See the real cost of A vs B lender

Calculate the total extra cost of going B-lender — and when the path to A-lender makes it worth it.

Bad Credit Doesn't Mean No Options in Calgary

A broker finds the path that works today — and builds the plan to get you to better rates tomorrow. Free, no obligation.