Mortgage Renewal · Calgary & Alberta

Mortgage Renewal Calgary — What to Do When the Letter Arrives

Your bank is betting you'll sign without shopping. A broker shops 50+ lenders and finds a better rate — free, in 48 hours.

- Switch lenders at renewal — no penalty, no stress test

- Typical savings: $3,000–$8,000 on a $400K mortgage over 5 years

- Rate hold for 120 days — start 4 months before your maturity date

- Broker fee paid by lender — free to you

What Happens at Mortgage Renewal in Alberta?

When your mortgage term ends, your lender sends a renewal offer — usually 45–120 days before maturity. You are not required to accept it. You can switch lenders, renegotiate your rate, or change your amortization at no penalty. Most borrowers sign without shopping — and overpay. An independent broker compares offers from 50+ lenders at no cost to you, and in most cases can secure a materially better rate than the bank's initial offer.

How Early Can You Start the Renewal Process in Alberta?

Most lenders allow you to lock in a new rate up to 120 days before your renewal date — without penalty. This means you can start comparing rates 4 months before your term ends. Rates can change daily. Starting early gives you the option to hold a rate while continuing to shop. Your broker monitors rates on your behalf and alerts you when it makes sense to lock in.

The Renewal Mistake Most Calgary Homeowners Make

When your renewal letter arrives, your bank is betting you'll sign and send it back without shopping around. Most people do — and it's the most expensive 10 minutes of their homeownership. Your bank's renewal offer is almost never their best rate. Brokers routinely beat it in 48 hours, for free.

What Happens at Mortgage Renewal in Calgary?

Your renewal letter is an offer, not a final answer. Here's exactly what to do.

Don't sign it yet

Your bank's renewal offer is their opening position. It's not their best rate. Treat it the same as any financial offer — with healthy skepticism and a counter.

Start shopping 4–6 months before your renewal date

Most lenders allow early renewal 120 days out with no penalty. Starting early means time to shop, compare, and lock in a rate hold without pressure.

Know your rights — switch lenders for free, no stress test

At renewal your mortgage contract has ended. You're free to move to any lender with no break penalty — and as of 2023, no stress test re-qualification required.

Talk to a broker — 48 hours, costs nothing

A broker shops 50+ lenders simultaneously, negotiates on your behalf, and presents your options side by side. The lender pays the broker fee. You pay nothing.

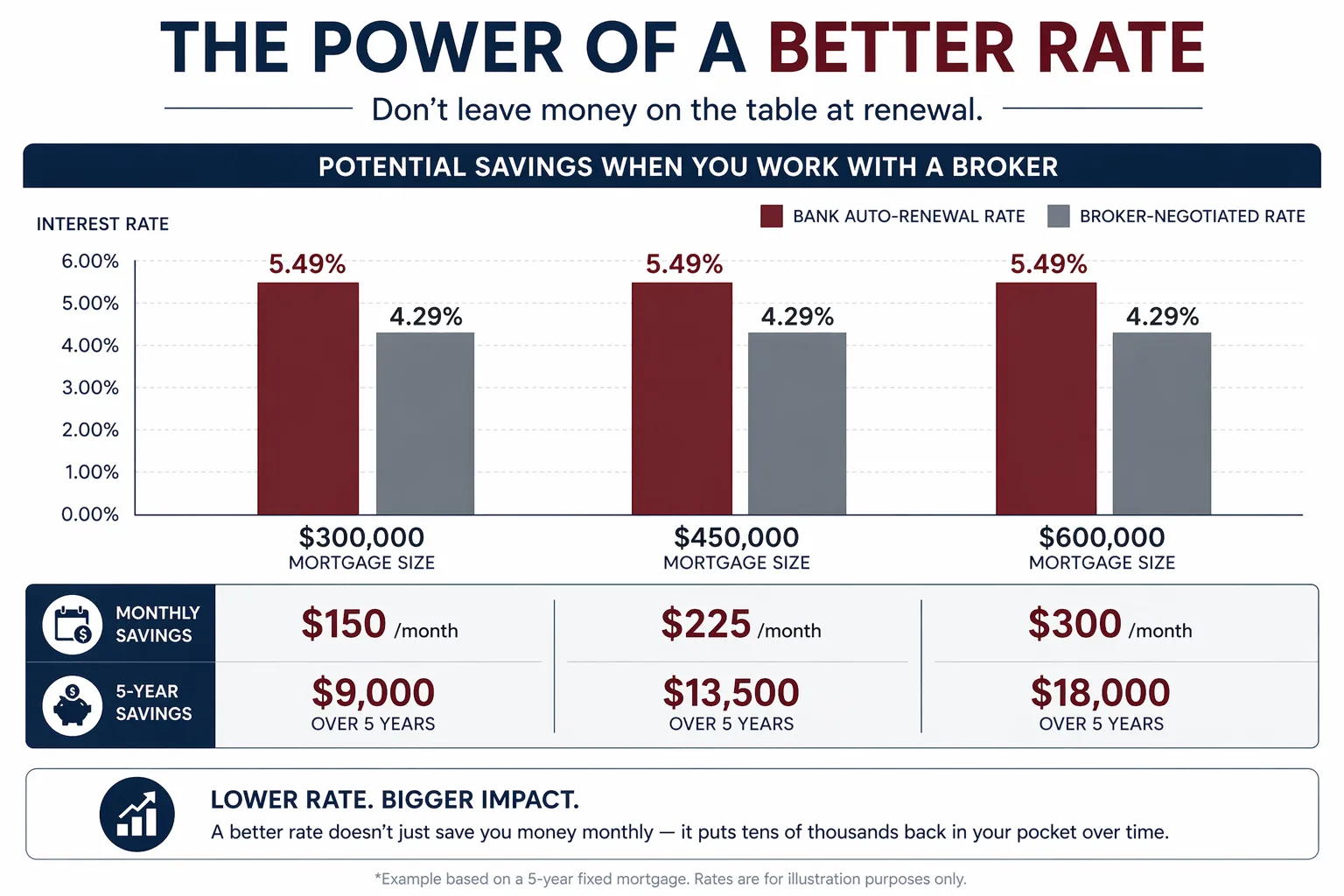

How Much Can You Save at Renewal?

Real Calgary numbers — based on typical broker vs bank rate differences.

Concrete Example — $400,000 Mortgage

Bank's renewal offer

5.39%

Posted rate — their opening position

Monthly payment: ~$2,420

Broker shopped rate

4.89%

Best available across 50+ lenders

Monthly payment: ~$2,300

Monthly saving

$120/month

Over 5-year term

$7,200 saved

Savings by Mortgage Size (0.5% rate improvement)

| Mortgage Balance | Monthly Saving | 5-Year Term Saving |

|---|---|---|

| $300,000 | ~$75/month | ~$4,500 |

| $400,000 | ~$100/month | ~$6,000 |

| $500,000 | ~$125/month | ~$7,500 |

| $600,000 | ~$150/month | ~$9,000 |

You Can Switch Lenders at Renewal — No Penalty, No Stress Test

At renewal your mortgage term has ended. You're free. And since 2023, you don't need to re-qualify with the stress test when you switch lenders — removing the last friction point banks relied on to keep you locked in.

No break penalty

Your term ended — there's nothing to break. Switching costs you nothing in penalties.

No stress test

Changed in 2023. You don't need to requalify at 6%+ just because you're changing lenders.

Legal costs often covered

Most lenders pay the legal and transfer costs to earn your mortgage. Standard practice.

Nothing else changes

You stay in your home. Same mortgage amount. Same amortization. Just a better rate.

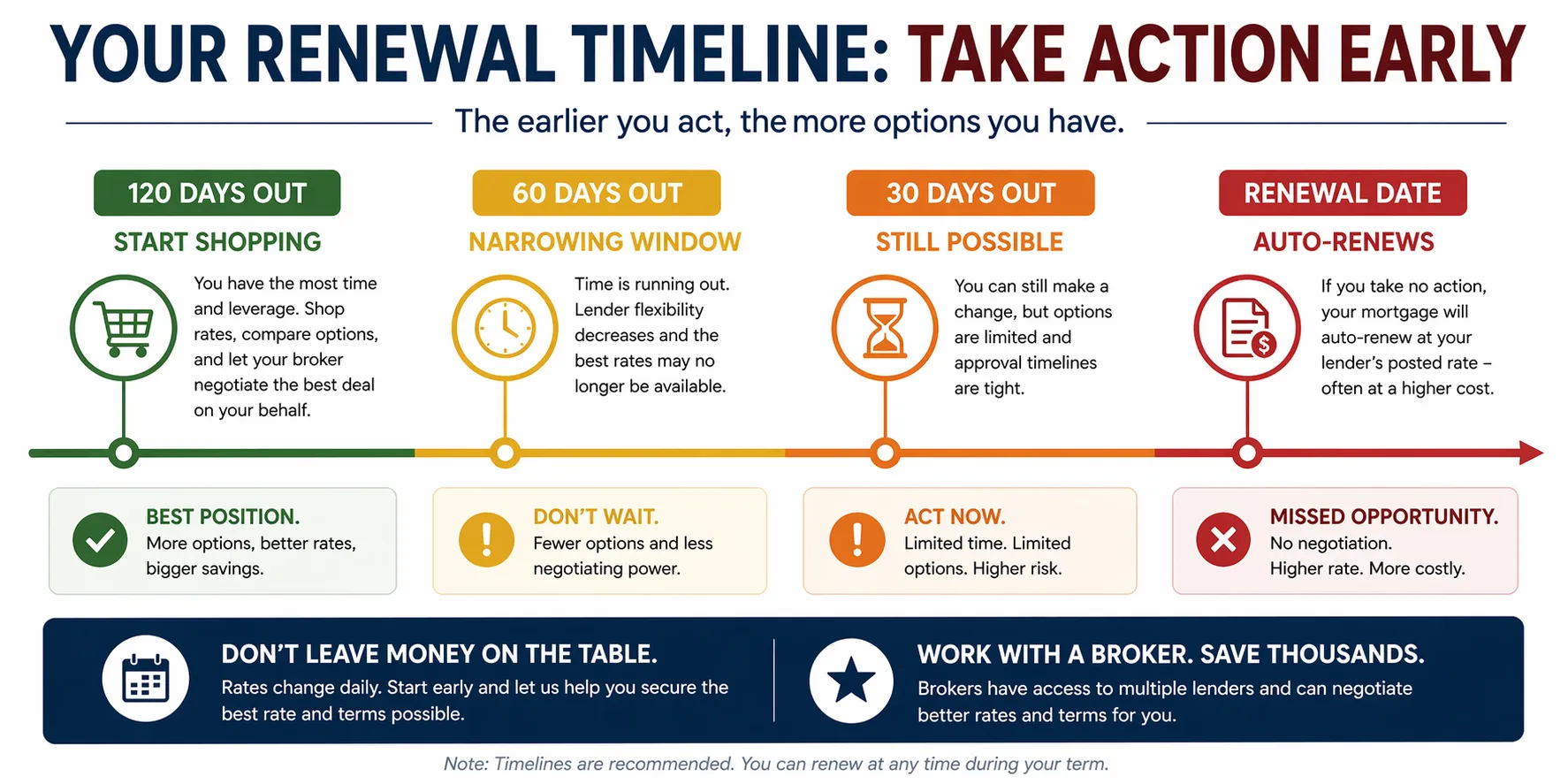

When to Start Shopping Your Renewal

Most lenders allow early renewal 120 days before your maturity date — with no penalty.

6 months out

Earliest window (some lenders)

A few lenders and credit unions allow 6-month early renewal. Ask your broker if this applies.

4 months out (120 days)

Standard early renewal window

Most major banks and monoline lenders. This is when your broker should be shopping actively. Lock in a rate hold.

90 days out

Still time, but pressure builds

Still penalty-free to switch. Rate holds give 120 days of protection from the date issued.

Renewal date

Auto-renews if you do nothing

If no action, your mortgage renews at whatever your bank offered. Avoid this outcome.

Rate holds last 120 days. Lock in a rate today — if rates rise before renewal, you're protected. If rates drop, your broker shops again. Upside protection with no downside.

Renewal is also a good time to review your protection coverage

Bank-provided creditor insurance is tied to your lender — if you switch at renewal, your coverage can lapse or require reapplication. Independent mortgage protection travels with you. Frank Cover is a Calgary independent insurance broker specializing in portable mortgage life and disability coverage across 20+ carriers.

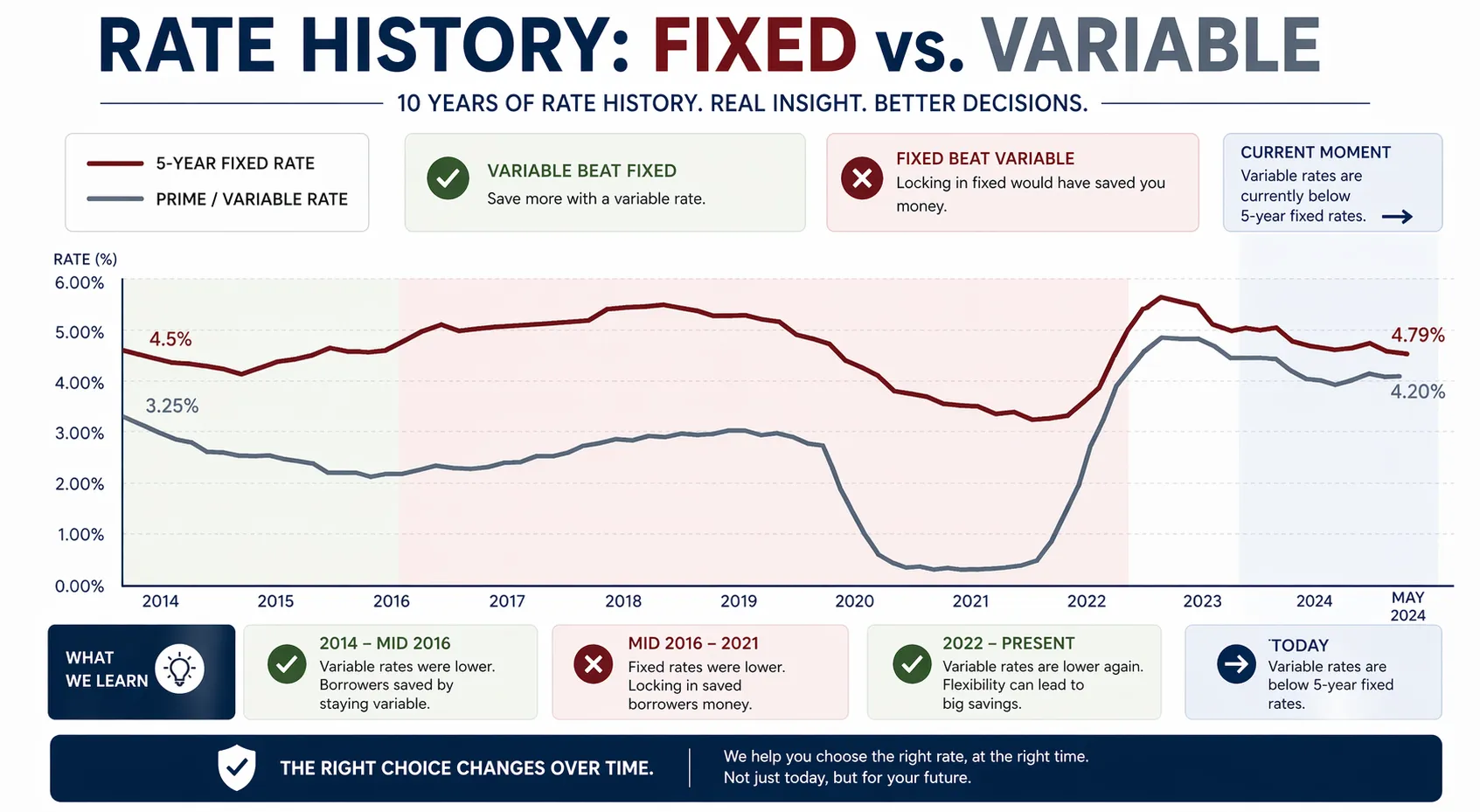

Fixed vs Variable at Renewal — What to Consider in 2026

Rates have come down from 2023 peaks. Here's how to think through your options.

5-Year Fixed

- Same payment for 5 years — no surprises

- Best for risk-averse or tight budgets

- Slight premium for predictability

- IRD penalty can be high if broken

3-Year Fixed

- Some rate movement without full variable risk

- Shorter commitment — renew sooner if rates drop

- Popular in 2025–2026 with rate uncertainty

- Lower IRD risk than 5-year

Variable Rate

- Prime minus 0.5–1.0% for strong borrowers

- Payments move with Bank of Canada

- Penalty always 3 months interest

- Best if rates expected to fall

Broker vs Your Bank at Renewal

Your bank has one interest at renewal: keeping your mortgage. A broker has one interest: finding you the best rate across 50+ lenders.

| Your Bank | A Mortgage Broker |

|---|---|

| 1 lender's products | 50+ lenders shopped simultaneously |

| Posted renewal rate (rarely best) | Negotiated rate, typically lower |

| No obligation to find you a better deal | Legally obligated to act in your interest |

| Doesn't mention switching is penalty-free | Explains all options, including switching |

| Costs nothing (but costs you more) | Costs you nothing — lender pays the fee |

Frequently Asked Questions

Mortgage Renewal Guides

Tactical articles on negotiation, switching lenders, and term selection.

How to Negotiate Your Renewal Rate

Step-by-step negotiation guide — what to say and when to walk away.

Switch Lenders at Renewal — No Penalty

The 2023 rule change and the penalty-free, stress-test-free switching process.

Fixed vs Variable at Renewal 2026

How to decide between terms in the current Alberta rate environment.

Mortgage Renewal Alberta

Province-wide guide to renewal strategy, lender options, and best rates.

Is breaking your mortgage early worth it?

Enter your balance, current rate, and new rate — get the break-even in seconds.

More Renewal Questions Answered

Your Renewal Is Too Important to Auto-Sign

Free 48-hour renewal review. No obligation. See what you actually qualify for across 50+ lenders.